What Is Full Retirement Age? A Complete Guide to Maximizing Your Social Security Benefits

Millions of Americans look forward to Social Security as a cornerstone of retirement income, yet many don’t fully understand how Full Retirement Age (FRA) impacts their monthly benefit. Claiming too early can permanently shrink your checks, while waiting strategically can boost them by 24% or more. In 2026, with FRA now solidly at 67 for those born in 1960 or later, understanding this key milestone has never been more important for U.S. workers planning their golden years.

The Motley Fool has long helped everyday investors make smarter financial decisions. This guide breaks down FRA, the trade-offs of different claiming ages, and proven strategies to get the most from your hard-earned benefits.

What Is Full Retirement Age (FRA)?

Full Retirement Age is the age at which you become eligible for 100% of your primary insurance amount (PIA)—the full monthly Social Security benefit calculated from your lifetime earnings. You can start collecting as early as age 62, but doing so triggers permanent reductions.

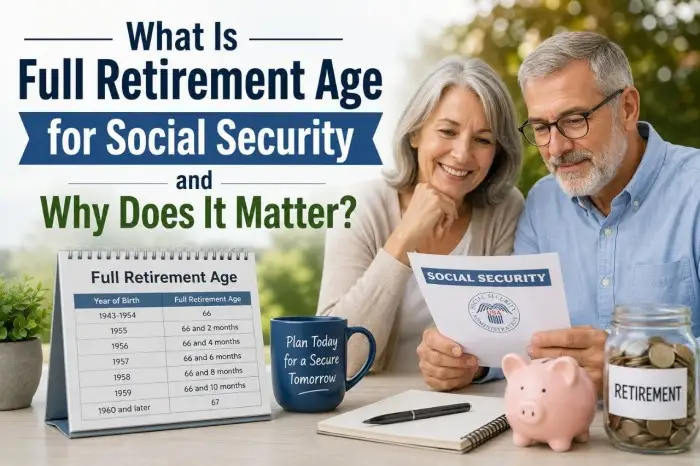

For 2026:

- If you were born in 1960 or later, your FRA is 67.

- For earlier birth years, FRA ranges from 66 to 66 and 10 months (for those born in 1959).

This gradual increase stems from 1983 legislation designed to extend the program’s solvency as Americans live longer. Medicare eligibility remains at 65, so many retirees bridge the gap with savings or part-time work.

Your exact FRA depends on your birth date. Use the official SSA Retirement Age Calculator for precision, but the rule is simple for most current workers: plan around age 67.

How Claiming Age Affects Your Benefit Amount

Social Security applies permanent reductions for early claiming and delayed retirement credits for waiting.

Claiming Before Full Retirement Age

You can file at 62, but benefits are reduced based on how many months early you start. For someone with FRA of 67:

- Claiming at 62 results in about a 30% permanent reduction.

- The reduction is roughly 5/9 of 1% per month for the first 36 months, then 5/12 of 1% thereafter.

Example: If your full benefit at FRA is $2,000 per month, claiming at 62 might drop it to around $1,400 for life. Early claiming also affects spousal and survivor benefits.

Claiming Exactly at Full Retirement Age

At FRA (67 in 2026 for most), you receive 100% of your calculated benefit with no reduction. This is the “neutral” point—no penalties, no bonuses.

Delaying Past Full Retirement Age

For every month you wait after FRA up to age 70, your benefit grows by delayed retirement credits—approximately 2/3 of 1% per month, or 8% per year.

- Waiting from 67 to 70 delivers a 24% increase.

- Maximum benefit occurs at 70; there’s no advantage to delaying further.

High earners who maxed out contributions could see the 2026 maximum monthly benefit exceed $4,000 at FRA, or significantly more at 70.

Strategies to Maximize Your Social Security Benefits

Smart planning goes beyond simply picking a number. Here are proven ways to increase lifetime income:

Work Longer and Earn More

Social Security bases your benefit on your 35 highest-earning years. Working past 62 (especially in higher-paying roles) can replace lower-earning years and raise your PIA. Even part-time work helps.

Delay Claiming If Possible

If you have sufficient savings, pensions, or other income, delaying until 70 often maximizes lifetime benefits—especially if you expect to live into your 80s or beyond. The Motley Fool analysis shows that for many healthy retirees, waiting pays off.

Coordinate with Your Spouse

Married couples have powerful options:

- One spouse claims at FRA while the other delays.

- Restricted application strategies (if eligible under older rules).

- Survivor benefits allow the surviving spouse to step up to the higher benefit.

Divorced individuals (married 10+ years) may claim on an ex-spouse’s record without affecting their benefit.

Understand Earnings Limits If You Work

In 2026, if you’re under FRA and still working, the earnings test applies:

- $24,480 limit (under FRA all year) — $1 withheld for every $2 over.

- Higher limit in the year you reach FRA.

Benefits withheld are not lost; they’re recalculated at FRA for a higher ongoing amount.

Minimize Taxes and Maximize Other Income Sources

Up to 85% of Social Security can be taxable depending on combined income. Roth conversions, strategic withdrawals, and health care planning (Medicare at 65) should align with your claiming decision.

Common Mistakes to Avoid

- Claiming at 62 out of fear the program will run out (it’s projected to pay ~75-80% even in worst-case scenarios after trust fund depletion).

- Ignoring spousal/survivor strategies.

- Forgetting that COLAs (cost-of-living adjustments) apply to your reduced or enhanced benefit.

Is There a One-Size-Fits-All Answer?

No. Healthy individuals with longevity in the family often benefit from delaying. Those with health concerns or needing income now may claim earlier. Use the SSA’s online tools, my Social Security account, or consult a financial advisor for personalized modeling.

The Motley Fool recommends running multiple scenarios with current earnings records. Small decisions today can mean thousands of extra dollars annually in retirement.

Take Control of Your Retirement Income

Full Retirement Age is more than a number—it’s the pivot point for one of your largest retirement assets. In 2026, with FRA at 67 for most workers, understanding reductions, credits, and maximization strategies can significantly improve your financial security.

Create your my Social Security account today, review your earnings record, and start planning. Whether you claim at 62, 67, or 70, an informed decision aligned with your health, savings, and lifestyle will help you enjoy retirement with greater confidence and less financial stress.

For more retirement insights and investing guidance trusted by millions of Americans, visit fool.com.